Note by James R. Martin, Ph.D., CMA

Professor Emeritus, University of South Florida

History and Development Main Page | Management

Theory Main Page

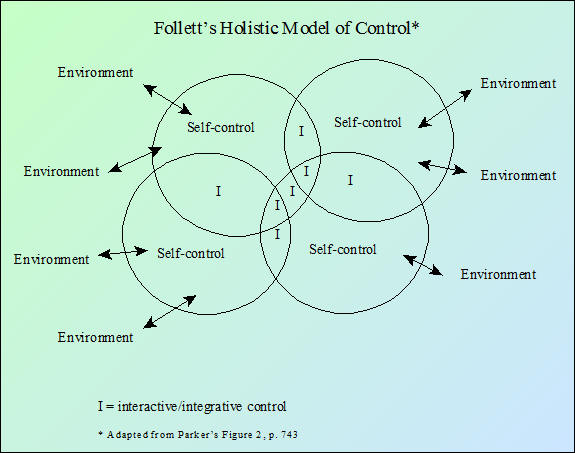

The purpose of this paper is to describe the work of Mary Parker Follett who built a bridge between the classical management control model and the behavioral and systems control models that were developed after 1960. Well in advance of the behavioral concepts of control Follett recognized the need for workers to exercise self-control and advocated that workers and managers should manage with each other. Organizations should allow collective self-control, two-way feedback of information, and lateral as well as vertical coordination of controls. She recognized that the organization could have a value greater than the sum of it's parts, and that it should focus on the operation of the whole system rather than the parts in isolation. Follett also stressed the interaction of individuals and groups with their environment. Her control model is illustrated below.

_____________________________________________

Some references to Follett's work:

Follett, M. P. 1937. The process of control. In L. Gulick & L. Urwick (eds.), Papers on the science of administration. Institute of Public Administration: 161-169.

Follett, M. P. 1941. The meaning of responsibility in business management. In H. C. Metcalf & L. Urwick (eds.), Dynamic administration: The collective papers of Mary Parker Follett. London: Sir Isaac Pitman & Sons Ltd., 146-166.

Follett, M. P. 1973. The psychology of control. In E. M. Fox & L. Urwick (eds.), Dynamic administration: The collected papers of Mary Parker Follett, 2nd edition. London: Pitman: 148-174

Related summaries:

Deming, W. E. 1993. The New Economics For Industry, Government & Education. Massachusetts Institute of Technology Center for Advanced Engineering Study. (Summary).

Dolk, D. R. and K. J. Euske. 1994. Model integration: Overcoming the stovepipe organization. Advances in Management Accounting (3): 197-212. (Summary).

Elliott, R. K. 1992. The third wave breaks on the shores of accounting. Accounting Horizons 6 (June): 61-85. (Summary).

Hammer, M. 1990. Reengineering work: Don't automate, obliterate. Harvard Business Review (July-August): 104-112. (Summary).

Johnson, H. T. and A. Broms. 2000. Profit Beyond Measure: Extraordinary Results through Attention to Work and People. The Free Press. (Summary).

Martin, J. R. Not dated. 200 years of accounting history dates and events. Management And Accounting Web. AccountingHistoryDatesAndEvents.htm

Martin, J. R. Not dated. Responsibility accounting compared to other concepts: Summary exhibits. Management And Accounting Web. ResponACCSum.htm

Martin, J. R. Not dated. Russell Ackoff: What is a system? Videos. Management And Accounting Web.RussellAckoffVideos.htm

Martin, J. R. Not dated. Simon's levers or control in relation to the balanced scorecard. Management And Accounting Web. Simon'sLeversofControl.htm

McNair, C. J. 1990. Interdependence and control: Traditional vs. activity-based responsibility accounting. Journal of Cost Management (Summer): 15-23. (Summary).