Summary by Antoinette L. Lynch

Ph.D. Program in Accounting

University of South Florida, Spring 2002

Behavioral Issues Main Page | Decision

Theory Main Page | Performance Measures Main Page

Purpose : The purpose of this study is to clarify the conflicting findings from earlier research regarding the impact of evaluating performance with accounting data. The study develops a research model from prior research findings designed to identify differences between positive and negative path individuals with respect the dimensions indicated in the research model. The study also evaluates the effectiveness of the performance report communication process.

Motivation: Generally, past research results have suggested that (1) negative attitudes toward budget, (2) a lack of influence in the budgetary process, and (3) perceptions of ambiguity are associated with negative motivation. For example, the results of prior research have indicated:

Managers, who were evaluated according to the budget, experienced less than favorable relationships with their supervisors and subordinates. Further, these same managers participated more in budget manipulation and misunderstood how the budget impacted their performance evaluation.

Managers, who disagreed with the appropriateness of their evaluation, experienced increased tension and encountered more job ambiguity.

Supervisors and their subordinates disagreed with each other regarding the performance criteria utilized in evaluations.

Poor job performance may result it evaluations are infrequent and/or unclear with respect to the individual’s performance on the job. In other words, the individual being evaluated may experience role ambiguity if there is a lack of clear information regarding the responsibilities and expectations of what constitutes effective performance.

Theory: Path-goal theory. Expectancy and instrumentality theory. Also, the authors rely on prior research to develop a research model. Prior research suggests:

Goals must be perceived as attainable in order to impact performance positively.

There is an indication that performance is better when goals are clear and quantitative.

Goals will only impact individual performance behavior to the extent that the individual accepts them.

Participation has been suggested as a way to improve motivation and performance.

Participation in the budgeting process leads to improved motivation, improved attitudes toward the job and organization, improved performance, and higher levels of job satisfaction under increased budget emphasis.

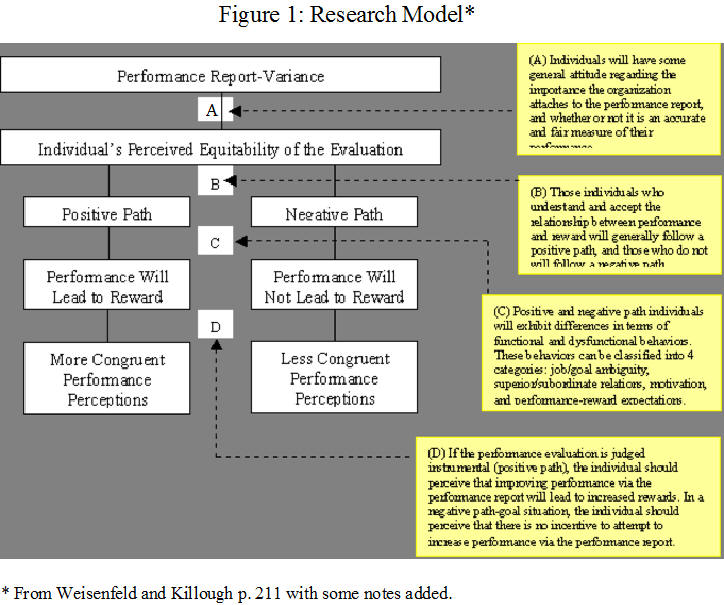

Research Model:

As indicated by the model, there is an assumption that to control performance, management requires a mechanism, which collects actual performance data and then compares it against a standard.

Hypothesis:

Individuals on a positive path would deem the performance report instrumental for improving performance and increasing their reward.

Performance ranking perceptions will increase for individuals on a positive path who deem the performance report instrumental for improving performance and increasing their reward.

Individuals on a negative path would not consider the performance report instrumental for improving performance and their reward.

Performance ranking perceptions will be less accurate for the negative path than the positive path.

Research Design and Setting:

Method: Field research

Questionnaires were developed to provide data for examining the differences between positive and negative path individuals.

The final questionnaire was administered on site by the researchers to upper, middle, and lower levels of plant management whose performance evaluation involved the use of variances.

Sample: Four plants, two from Company A (45 respondents) and two from Company B (33 respondents), in furniture manufacturing industry and located in the same general geographic area. Each of the plants was under a tight monitoring system based on variances reports. For both companies, upper levels of plant management were well aware of the problems that might exist in middle and lower levels with respect to standards and operating variances. In general, both companies appeared to use variances in a positive manner to monitor and control operations rather than trying to use them in some sort of punitive manner.

Results:

Relationship B was used to identify respondents indicating a positive or negative path with respect to the performance report variances. However, comparisons between the two paths are limited due to a lack of respondents in the negative path category (66 positive, 2 negative, and 10 unclassified).

As stated by the authors, in general, the results of this study appear to indicate that the use of performance report variances should promote functional behavior under the following circumstances:

1. Managers are in agreement regarding how they evaluate and how they are evaluated (congruency exists).

2. The performance report is perceived as appropriate and fair.

3. Managers understand that their reward is tied to their performance as measured by the performance report variances.

4. The jobs or goals promoted by the performance report are not ambiguous.

5. The tasks or goals promoted by the performance report are not ambiguous.

6. The tasks being measured are relatively certain.

Performance report variance information facilitates more agreement if individuals are on a positive path.

To move individuals from the negative path to the positive path, superiors should be encouraged to discuss the goals represented by the performance report, emphasize the importance of the variances with respect to performance valuation and bonus, and promote an open participative atmosphere with respect to performance and evaluation.

Superior/subordinate communication process is the key to the success when using performance report variances for the promotion of functional behavior.

Unlike the results of prior research, this study indicated that superiors and subordinates were aware of how they were evaluated as well as how they evaluated their subordinates. They generally were also in agreement regarding the extent to which the performance report variances were emphasized.

The managers in this study felt that the performance report was an appropriate way to measure their performance.

__________________________________________________

Related summaries:

Fullerton, R. R. 2003. Performance measurement and reward systems in JIT and non-JIT firms. Cost Management (November/December): 40-47. (Summary).

Fullerton, R. R. and C. S. McWatters. 2002. The role of performance measures and incentive systems in relation to the degree of JIT implementation. Accounting, Organizations and Society 27(8): 711-735. (Summary).

Nicholson, N. 2003. How to motivate your problem people. Harvard Business Review (January): 57-64. (Summary).

Scott, T. W. and P. Tiessen. 1999. Performance measurement and managerial teams. Accounting, Organizations and Society 24(3): 263-285. (Summary).

Shields, M. D., F. J. Deng and Y. Kato. 2000. The design and effects of control systems: Tests of direct- and indirect-effects. Accounting, Organizations and Society 25(2): 185-202. (Summary).

Simons, R. 1995. Control in an age of empowerment. Harvard Business Review (March-April): 80-88. (Summary).

Stevens, T. 1994. Dr. Deming: Management today does not know what its job is. Industry Week (January 17): 21, 24, 26, 28. (Summary).

Tongtharadol, V., J. H. Reneau and S. G. West. 1991. Factors influencing supervisor's responses to subordinate's poor performance: An attributional analysis. Journal of Management Accounting Research (3): 194-212. (Summary).

Van der Stede, W. A. 2000. The relationship between two consequences of budgetary controls: Budgetary slack creation and managerial short-term orientation. Accounting, Organizations and Society 25(6): 609-622. (Summary).

Walker, K. B. and E. N. Johnson. 1999. The effects of a budget-based incentive compensation scheme on the budgeting behavior of managers and subordinates. Journal of Management Accounting Research (11): 1-28. (Summary).